basilh@stanford.edu

@basilhalperin

In 2008, Christina and David Romer published an interesting paper demonstrating that FOMC members are useless at forecasting economic conditions compared to the Board of Governors staff, and presented some evidence that mistaken FOMC economic forecasts were correlated with monetary policy shocks.

I've updated their work with another decade of data, and find that while the FOMC remained bad at forecasting over the extended period, the poor forecasting was not correlated with monetary policy shocks.

First, some background.

Background

Before every FOMC meeting, the staff at the Board of Governors produces the Greenbook, an in-depth analysis of current domestic and international economic conditions and, importantly for us, forecasts of all kinds of economic indicators a year or two out. The Greenbook is only released to the public with a major lag, so the last data we have is from 2007.

The FOMC members – the governors and regional bank presidents – prepare consensus economic forecasts twice a year, usually February and July, as part of the Monetary Policy Report they must submit to Congress. (Since October 2007, FOMC members have prepared projections at four FOMC meetings per year. That data, from the end of 2007, is not included in my dataset here, but I'll probably put it in when I update it in the future as more recent Greenbooks are released.)

Summary of Romer and Romer (2008)

The Romers took around 20 years of data from these two sources, from 1979 to 2001, and compared FOMC forecasts to staff forecasts. They estimate a regression of the form

Where X is the realized value of the variable (e.g. actual GDP growth in year t+1), S is the staff's projection of the variable (e.g. the staff's projected GDP growth next year), and P is the FOMC's projection of the variable (e.g. the FOMC's projected GDP growth next year).

They find "not just that FOMC members fail to add information, but that their efforts to do so are counterproductive." Policymakers were no good at forecasting over this period.

They then ask if the mistaken forecasts cause the FOMC to make monetary policy errors that cause monetary policy shocks. The two use their own Romer and Romer (2004) measure, which I've updated here, as the measure of monetary policy shocks. They then estimate the regression

Where M is the measure of shocks, and P and S are as before. They only ran this regression from 1979 through 1996, as that was the latest the measure of shocks went up to in the 2004 paper.

They find that, "The estimates suggest that forecast differences may be one source of monetary shocks... An FOMC forecast of inflation one percentage point higher than the staff forecast is associated with an unusual rise in the federal funds rate of approximately 30 basis points."

That seemed like a very interesting result to me when I first read this paper. Could bad monetary policymaking be explained by the hubris of policymakers who thought they could forecast economic conditions better than the staff? It turns out, after I updated the data, this result does not hold.

Updating the data

I followed the same methodology as when I updated Romer and Romer (2004): first replicating the data to ensure I had the correct method before collecting the new data and updating. The data is from 1979 through 2007, and all my work is available here and here.

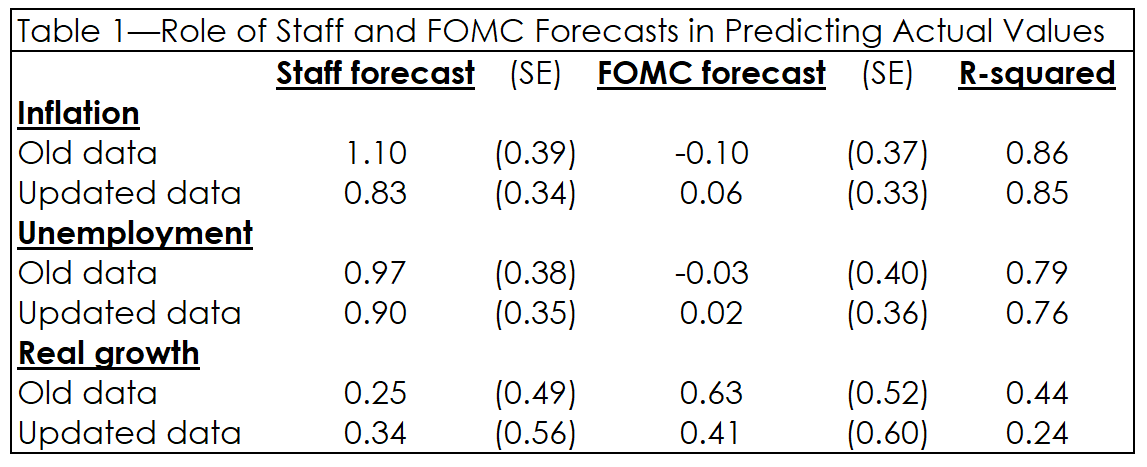

I find, first, that policymakers remained quite poor economic forecasters. Here is the updated version of Table 1 from the paper, with the old values for comparison:

The coefficient on the FOMC forecast for inflation and unemployment is still right around zero, indicating that FOMC forecasts for these two variables contain no useful information.

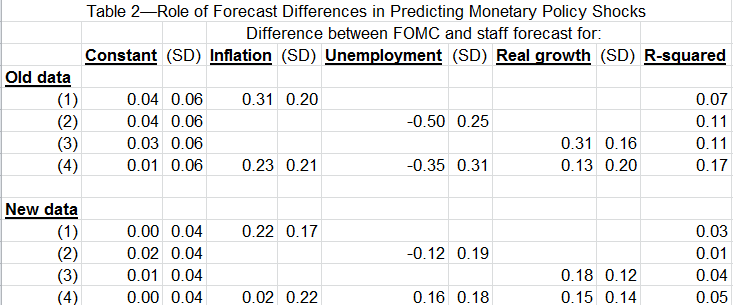

However, it appears that once we extend the monetary policy shock regression from 1996 to 2007, the second result – that forecast differences are a source of monetary policy shocks – does not hold. Here is the updated version of Table 2 from the paper, again with old values for comparison:

When the Romers published their paper, the R-squared on the regression of monetary shocks over all three variables was 0.17. This wasn't exactly the strongest correlation, but for the social sciences it's not bad, especially considering that monetary shock measure is fairly ad hoc.

As we can see in the updated regression, the R-squared is down to 0.05 with the extended data. This is just too small to be labeled significant. Thus, unfortunately, this result does not appear to hold.